Starting salaries have struggled to keep up with the rising cost of living in recent years.

An older friend once shared with me that back in the year 2000, he and his wife had a combined income of $5,000. With that, they could comfortably afford a 5-room resale flat and a car. For many of us in the younger generation, such opportunities feel out of reach.

It’s no surprise, then, that having sufficient income remains the top concern for Millennials in Singapore, as highlighted in a 2019 Blackrock survey.

This desire to increase our take-home pay isn’t just about wanting more—it’s driven by the many financial responsibilities we juggle.

From providing for ageing parents and saving for retirement to buying a home, starting a family, and improving our immediate quality of life, there’s no shortage of competing priorities.

The challenges are real, but they also reflect our aspirations for a better future—for ourselves and for the people we care about.

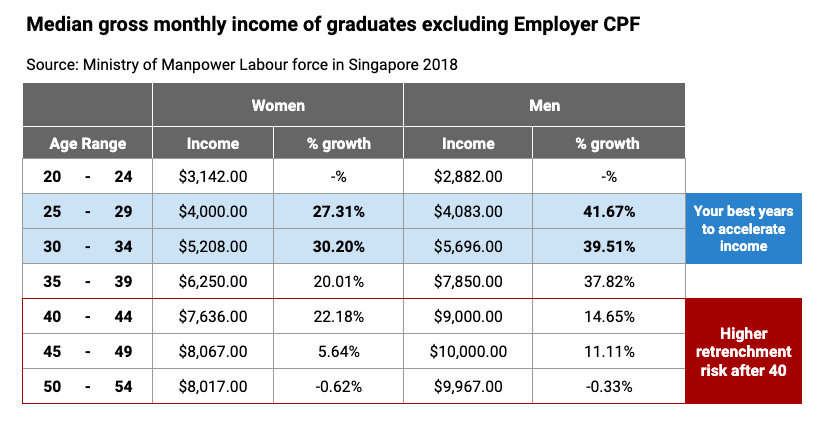

The good news is that we’re at a stage in life where we can grow our salaries the most.

Looking at the data, the ages of 25–34 represent the period when income tends to increase most significantly. This trend is consistent across developed countries, where income growth typically slows after the first 10 years of a career.

While there’s still potential for growth between 35–39 years old, I’d strongly encourage focusing on building wealth and increasing your income during your 20s and early 30s.

After 40, the challenges can become steeper. The risk of retrenchment rises, financial obligations—such as supporting elderly parents, raising children, and managing other expenses—become heavier, and health issues may lead to unexpected costs.

In my own journey, I’ve managed to grow my annual income significantly over the first five years of work. This has helped me build a solid savings foundation before turning 30.

I’d like to share some tips that have worked well for me in the hope that you might find them helpful too.

Please note that my experience is based on being a full-time employee in a PMET role with a degree, so it may not fully apply to those in different career paths, such as freelancers, entrepreneurs, or those in non-PMET roles.

1. Perceive yourself as a business, not an employee

Career growth begins first with the mindset. The key is to manage your career as if it were a start-up business: a living, breathing, growing start-up of you.

In other words, do not see yourself as ‘Employee’ but your own one-man business who is selling time, skills and performance to a company.

This advice was shared by Reid Hoffman, Founder of LinkedIn in his book The Start-up of You: Adapt to the Future, Invest in Yourself, and Transform Your Career. While the book is written 8 years ago, I feel that it is highly relevant to us even till today.

Just like how a business thinks about Year-on-year growth, your focus should not only be on how you can help your company grow but more of how you can help yourself achieve salary growth year-on-year.

Start by track your Year-on-year salary growth in a spreadsheet (If you forgot, you can refer to IRAS website), set goals and hold yourself accountable. You can refer to the chart above to benchmark your growth with other Singaporeans but do not let gender be a limit to your potential.

Like how a company invests in assets and innovation, your focus can also be on investing in yourself by by building skills. Some examples include volunteer to do things which will help you pivot into your next play; Pick up learning after working hours and use your SkillsFuture credit to learn a new language.

Learning how to invest is an important skill but don’t neglect investing in your ‘human capital’ especially in your youth when your earned income from work tends to far exceed your income from investments for most people

Unfortunately, for far too many, focused learning ends at college graduation. They read about stocks and bonds instead of reading books that improve their mind. They compare their cash salary to their peers’ instead of comparing lessons learned. They invest in the stock market and neglect investing in themselves. They focus, in short, on hard assets instead of soft assets. This is a mistake.

Reid Hoffman

2. Build valuable skills and join high growth companies

The best way to accelerate your income is to build a valuable set of skills which are short in supply.

The labour market works the same way as our economy does – Demand and supply. In high growth industries, generally, the demand for people with specific set of skills outweigh the supply available. Hence, companies tend to be more willing to provide high salaries and more benefits.

Sometimes, even in industries that are not growing fast, the pay can be decent as a result of demand exceeding supply of talent. For instance, some professions like entry-level Commercial Pilots pay well ($6,500 to $10,000) due to the shortage of pilots.

This view is also shared by Managing director of recruitment agency Robert Half Singapore, Matthieu Imbert-Bouchard who shared that pay raises were most often given to staff in specialised positions with low talent supply because “employers understand they need to offer above-average salaries and pay rises in order to secure and retain staff”

In contrast, he observed that for the rest of Singapore, obtaining a pay rise would be “challenging”, as employers were reluctant to meet salary requests given the negative economic forecast for the coming year.

In addition to building valuable skills, you can also look out for companies with consistently high growth.

In his book “Earn What You’re Really Worth“, author Brian Tracy also pointed out 20 percent of the companies in any industry make 80 percent of the profits. These companies have better leadership, better products and services, better technology, and a better future. These are the companies which you want to work.

This is true. When companies grow quickly, opportunities surface everywhere whether it is to get promoted or make a lateral move.

If you would not invest your money in a company with poor or negative growth, why join one in the first place? Furthermore, if a company cannot even grow 20 percent on their own, how can they comfortably afford to give you a 20 percent pay rise?

3. Stay on top of your market rate

Early in my career, I learnt that a colleague was earning more than me despite graduating at the same time for the same role and same KPIs. I was upset to learn that I was underpaid and started looking out.

From there, I made it a point to always stay informed about the market rate so that I can ensure my compensation stays aligned with the value I bring

To some, it may seem calculative. However, doing so also ensures you will not be shortchanged. For instance, there are many business development representative roles in the market but not all are made equal. Assuming the targets are similar, if one offers capped commissions at $1,500-$2,000 but the other one has uncapped commissions, why not explore the other position? Who is to say the pace, type of colleagues and workload will be any worse?

In this day and age, getting publicly available salary information is also quite easy.

For all the flaws of MyCareersFuture.sg, the website is a really good asset to Singaporeans in one critical way – most of their jobs have salary information tied to it. Simply search the company name or job title on the website and you will be able to find the list of jobs as well as the salary range they are offering for the role.

Besides public sources, you can also leverage recruiters on LinkedIn or sign up for mailing list of recruiters. I have peers who speak to recruiters even when they are not actively looking, just to get a sense of their market rate and stay on top of opportunities available.

The most accurate source will be your peers in the same industry. Unlike previous generations, millennials are generally more open about such information.

Many millennials believe that sharing allows them to hold their company accountable for fair pay practices and ensure they are getting paid what they are worth. If they are not a first, typically, people start sharing after a few drinks. 😉

In your pursuit of income increase, do watch out for those employers who use “passion” as a means to exploit you.

They may say things like “passion” is more important than money and use it as a reason to under pay you but make you put more effort. Or, glorify and award those who put in long hours. This is quite common especially among creative industries and some start-ups with ‘cult-like’ culture.

In many of these cases, “Doing what you love” has been co-opted by corporate interests, giving employers more power to exploit their workers.

In fact, researchers found that people consider it more legitimate to exploit passionate employees i.e. make them leave family to work on a weekend, work unpaid, and handle unrelated tasks that were not in the job description. After all, if you truly love what you do, pedestrian concerns about salary, health care, and retirement savings can take a back seat. Passion and devotion are what matter.

These ideas were shared by Miya Tokumitsu who has studied and written extensively about the cultural values that work holds in the twenty-first century in her book Do What You Love And Other Lies About Success and Happiness.

4. Pick a job where compensation is aligned to performance

One way to accelerate your earnings is to pick a job where bonuses are tied to actual performance.

The last thing you want is to have spent the entire year putting in extra hours, meeting KPIs and going the extra mile but only to be told Everyone in this company works hard and goes the extra mile” or “We can’t give you a pay raise because of *inconsequential flaw that you have*.”

Some companies also have rules like “Oh, everyone in their first year is going to get a B- grade. Otherwise, those who worked in the company for a long time will be angry!”

This simply means no matter how hard you work, your bonus will be the same as someone lazier. If your goal is to grow your income, this is may be something you want to avoid.

If you have a larger risk appetite, you may also opt for startups. Many high growth startups give good bonuses and even equity. This also ties in with the first point raised about joining high growth companies as they can generally give better bonuses.

5. Performance is not everything – Relationships are

When I first started working, I naively believed that success was all about hitting my KPIs. I thought that as long as I exceeded expectations, everything else would naturally fall into place.

Looking back, I now realize how much I overlooked the importance of managing relationships—both with my superiors and my peers.

In the early days of my career, I was too vocal. I did not understand how much a superior’s opinion of you could impact your career—your pay, your promotions, and even your day-to-day work experience.

It wasn’t until later that I learned an important truth: even if you consistently hit your KPIs, a superior who doesn’t like you will still find reasons to focus on your shortcomings.

Building strong relationships with colleagues matters just as much. In recent years, I’ve come to appreciate that “Goodwill is more important than glory.” While performance and relationships aren’t mutually exclusive, I’ve learned that it’s often better to be third place in performance and have strong, supportive relationships than to be first place but lack those connections.

These lessons didn’t come easily, but they’ve shaped the way I approach work today. For anyone just starting their career, I’d encourage you to think not just about results but also about how you work with and relate to the people around you.

Success, I’ve learned, is as much about people as it is about performance.

While income from work is just one piece of the wealth-building puzzle, it plays a critical role—especially in our early years.

These formative years are our runway. They give us the chance to build capital, harness the power of compound interest, and develop habits that lay the foundation for long-term financial freedom.

By being intentional early on—earning, saving, investing—we increase our chances of stepping off the treadmill sooner. But it’s not just about escaping the rat race. It’s about designing a life on our own terms.

A life where we have the freedom to give back to the causes we believe in, spend more meaningful time with the people we love, and pursue what truly matters—with clarity and confidence.

Financial freedom isn’t just a number. It’s a mindset and a means to live with purpose.